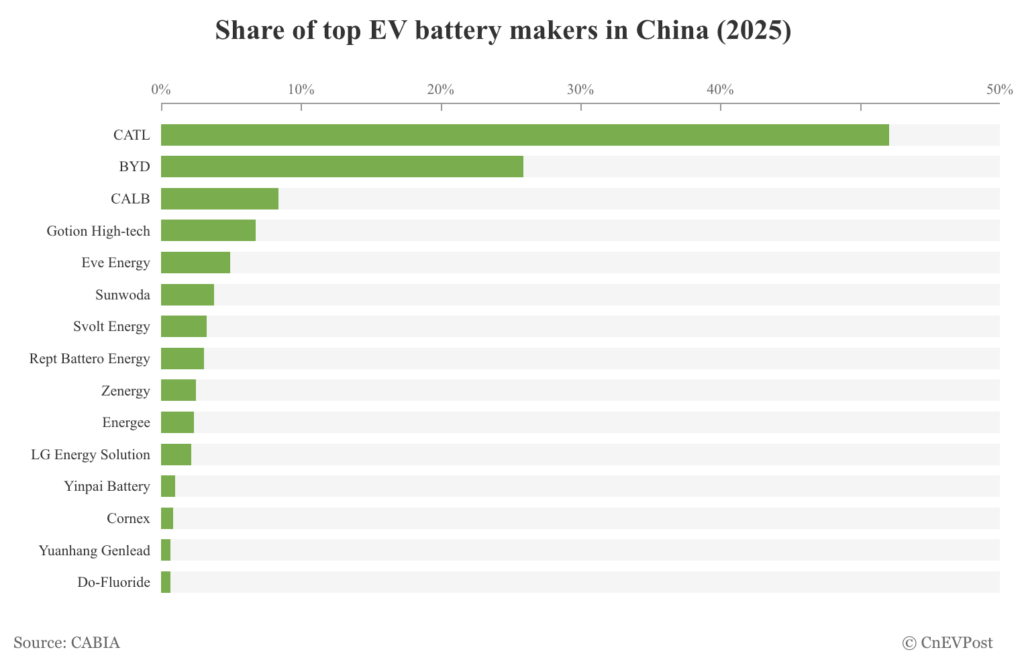

Contemporary Amperex Technology Co., Limited (CATL) maintained its leading position, installing 333.57 GWh of batteries in China last year—enough to power approximately 5.07 million vehicles—equating to a 43.42% share of the domestic market, down slightly from 45.08% in 2024. Second-place BYD registered 165.77 GWh of installations, powering 3.82 million vehicles and capturing 21.58% of the market, a decline from 24.74% in 2024.

In third place, CALB installed 53.61 GWh of power batteries, supplying 830,000 vehicles and securing a 6.98% share, up from 6.68% in the previous year. Gotion High-tech and Eve Energy followed with 43.44 GWh (5.65% market share) and 31.61 GWh (4.11%), respectively. Other notable contributors included Sunwoda (24.35 GWh, 3.17%), Svolt Energy (20.71 GWh, 2.70%) and Rept Battero Energy (19.50 GWh, 2.54%).

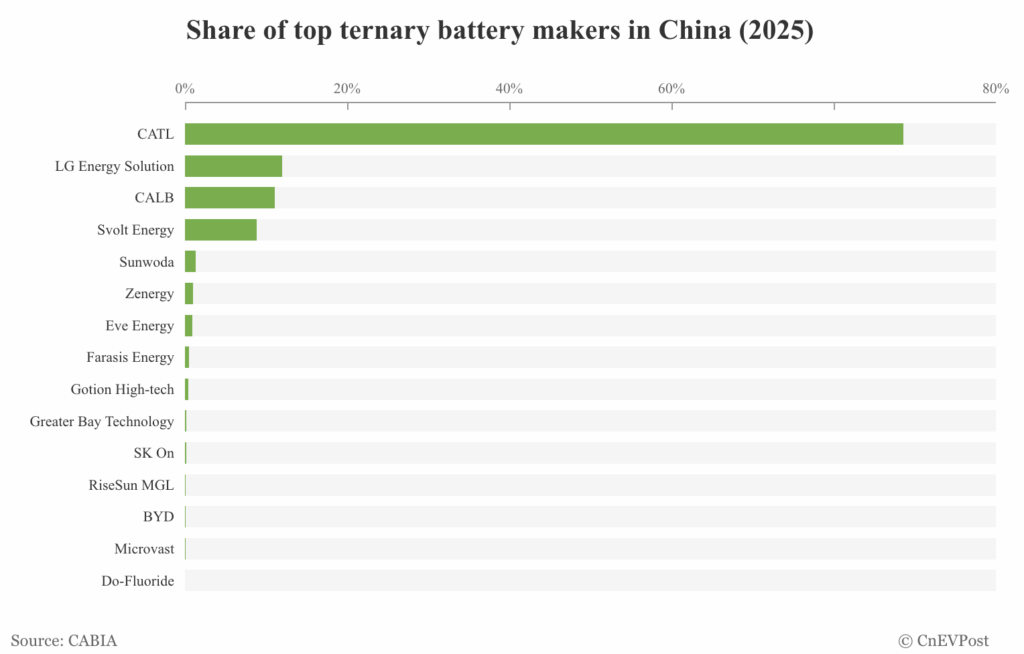

In the ternary (nickel-manganese-cobalt) segment, CATL accounted for 101.61 GWh—70.90% of the market and a gain of 1.67 percentage points year-on-year—sufficient for around 1.46 million vehicles. LG Energy Solution held the second spot with 13.75 GWh (9.59%), followed by CALB at 12.73 GWh (8.88%).

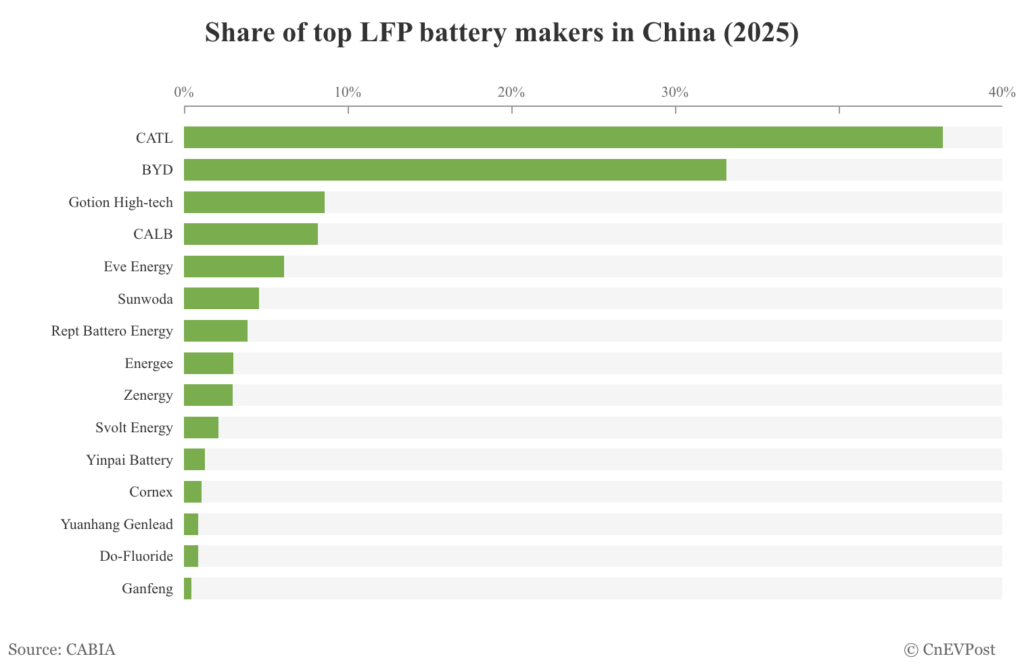

Within the LFP category, CATL again led with 231.96 GWh (37.10% of the segment), powering 3.61 million vehicles. BYD came in second with 165.74 GWh (26.51%), while Gotion High-tech ranked third, installing 42.94 GWh (6.87%). Other participants in the LFP market included CALB, Eve Energy and Sunwoda.

Overall, the data highlight the dominance of CATL and BYD in China’s expanding EV battery industry, alongside steady gains from several domestic manufacturers.

Source: CnEVPost