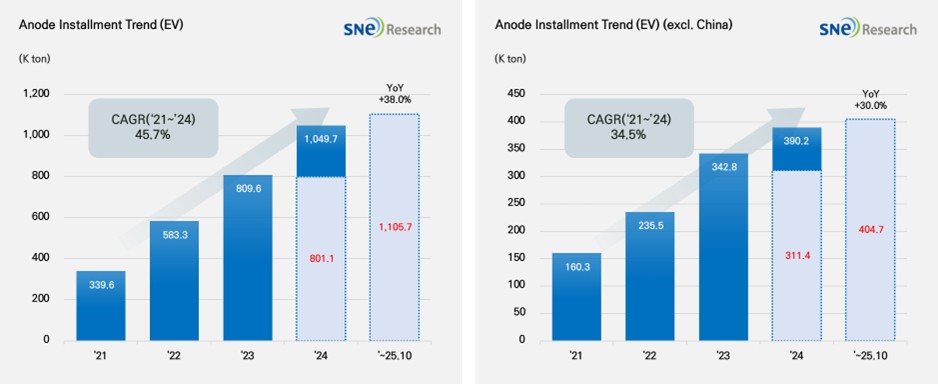

From January to October 2025, global installations of anode materials for electric vehicles—including battery electric, plug-in hybrid, and hybrid models—reached approximately 1.106 million metric tons, representing a 38.0% year-over-year increase. In markets outside China, installations amounted to 405,000 metric tons, up 30.0% from the same period in 2024. This sustained growth reflects continued expansion in electric mobility worldwide.

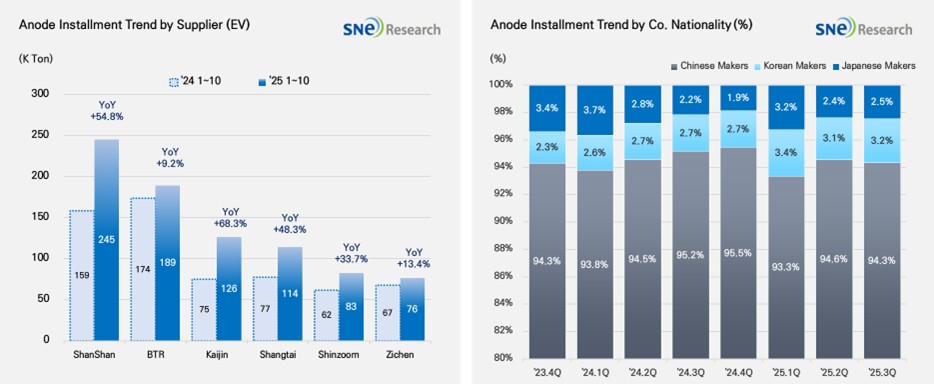

Market-share data indicate that Chinese producers dominate the sector, accounting for more than 94% of global anode shipments. Leading the pack are ShanShan, with 245,000 metric tons, and BTR, at 189,000 metric tons; both companies supply major cell manufacturers. Other fast-growing suppliers include Kaijin (126,000 metric tons), Shangtai (114,000 metric tons), Shinzoom (83,000 metric tons), and Zichen (76,000 metric tons), each posting double-digit annual growth.

Korean anode makers hold around 3.2% of the market, with POSCO and Daejoo expanding partnerships with cell producers in North America and Europe. Japanese firms account for roughly 2.5% of global share, with established companies such as Hitachi and Mitsubishi maintaining conservative approaches focused on existing customers.

Industry observers note that 2025 represents a structural inflection point for anode materials, as supply-chain risks and technology transitions coincide with a recent price rebound. The United States has announced preliminary anti-dumping and countervailing duties on Chinese anode imports, while China has imposed—and then partially deferred—export licensing requirements on high-purity synthetic and natural graphite and certain battery components. These developments have prompted buyers in North America and Europe to accelerate efforts to diversify sources, though replacing China’s capacity in the near term remains challenging.

Looking ahead, rising anode costs may drive up battery prices through 2026–2027. Cell manufacturers and automakers are expected to include raw-material price indexation clauses in long-term contracts and allocate a portion of regional volumes to non-Chinese suppliers. At the same time, silicon-carbon composite anodes are emerging as a promising alternative. Korean materials companies that align technology development with diversified supply chains could turn this transition phase into a new growth opportunity.

Source: SNE Research