Welcome back to this week’s Battery Business Insights article on Europe’s most significant industrial policy shift in decades. On March 4, 2026, the European Commission unveiled the Industrial Accelerator Act, a framework that could transform how batteries are manufactured, procured, and deployed across the European Union. The legislation introduces Made in EU requirements for battery energy storage systems and electric vehicles, targeting strategic independence from suppliers that currently dominate global production. With China controlling over 80% of global battery manufacturing capacity, the IAA represents Europe’s most assertive response to supply chain vulnerabilities that threaten both its energy transition and industrial competitiveness.

By the Numbers: The IAA’s Battery Provisions

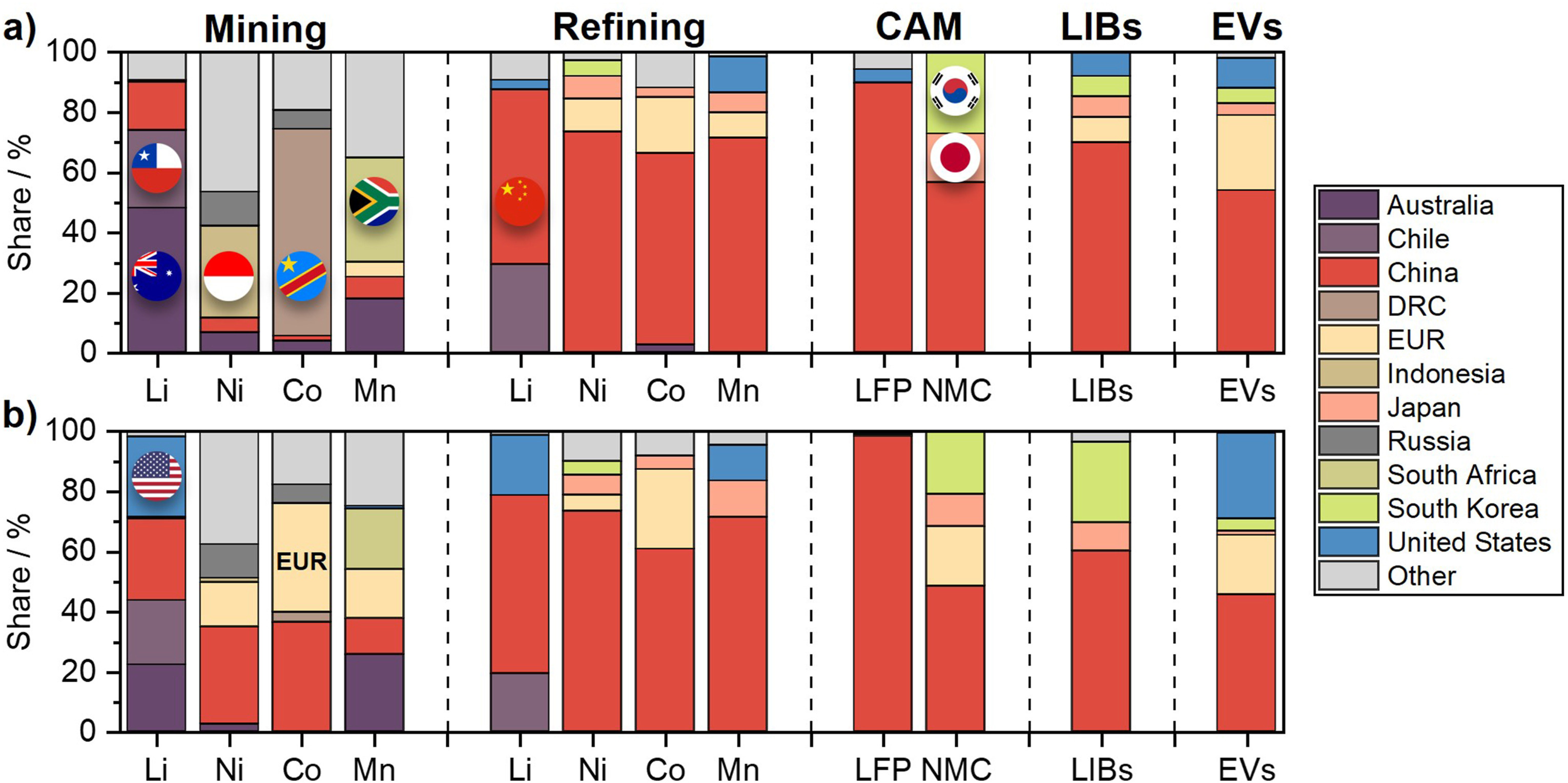

- 80%: China’s share of global battery and solar photovoltaic manufacturing capacity

- 90%: Current cost premium for EU battery cells compared to Chinese production, equivalent to $41-43/kWh

- 30%: Projected cost gap by 2030 if the IAA drives scale and efficiency improvements, reducing the difference to approximately $14/kWh

- €500: Expected “sovereignty premium” per electric vehicle by 2030 due to higher EU battery costs

- 66%: Share of electric cars sold in the EU that will require European-made batteries starting in 2027

- 70%: Minimum EU-origin content (excluding batteries) required for electric vehicles receiving public support

- 85,000: Battery sector jobs the IAA is projected to create or preserve

- €10.5 billion: Expected added value across the automotive value chain

- 30.58 million tonnes: Projected CO₂ savings in energy-intensive industries

- 125 vs. 35: Workers per GWh of battery production in Europe compared to China

How Europe Lost Ground in Battery Manufacturing

Europe’s battery manufacturing sector has struggled to compete with Asia for decades. While the continent maintained strength in automotive engineering and chemical industries, it missed the lithium-ion battery revolution that began in the 1990s. By 2026, China has built an unassailable lead, with companies like CATL supplying roughly one-third of all EV batteries worldwide. European battery production relies on projects like Spain’s €4 billion gigafactory, which required 2,000 Chinese workers for construction and aims for just 50 GWh annual capacity by 2030.

The cost disadvantage stems from fundamental inefficiencies. European battery facilities employ 125 workers per GWh of production capacity, compared to 35 in China. Higher scrap rates, lower automation levels, and elevated electricity costs compound the problem. Currently, only 68% of battery value is generated locally in Europe, with less than 31% of cathodes sourced from European suppliers. The rest depends on Chinese supply chains for critical materials and components.

The Net Zero Industry Act, adopted in 2024, set aspirational targets for domestic production but lacked enforcement mechanisms. Companies continued sourcing from China because it remained cheaper, leaving European battery manufacturers struggling to secure offtake agreements with automakers. The Industrial Accelerator Act represents a shift from voluntary goals to mandatory requirements, using public procurement and state aid as leverage to create lead markets for European production.

The IAA’s Phased Battery Requirements

The Industrial Accelerator Act introduces a two-stage timeline for battery energy storage systems. From one year after entry into force, BESS must originate in the EU. Systems larger than 1 MWh must include an EU-made battery management system. From three years after entry into force, systems must additionally include EU-manufactured battery cells and at least one main specific component.

For electric vehicles, the requirements operate differently. Vehicles receiving public support must be assembled in the EU with at least 70% of their components, excluding the battery, manufactured in EU Member States. From 2027, almost two-thirds of electric cars sold in the EU will be required to have batteries produced in Europe under local content rules tied to CO₂ emission performance standards.

Industrial Accelerator Act: Key Battery Industry Numbers

The legislation also imposes conditions on foreign direct investment. Investments exceeding €100 million in strategic sectors, including batteries, require approval when a single third country controls more than 40% of global manufacturing capacity. This threshold directly targets Chinese battery manufacturers, who must now guarantee a 50% minimum level of European employment, technology transfer, and compliance with local content requirements to access European subsidies or trade benefits.

The Commission frames the IAA as an “insurance policy” for strategic economic independence. It aims to increase manufacturing’s share of EU GDP from 14.3% to 20% by 2035, reversing decades of decline. The battery sector represents a central pillar of this strategy, given its role in electric mobility, renewable energy storage, and industrial decarbonization.

Industrial Accelerator Act Timeline

Year 1

Battery Energy Storage Systems must originate in the EU.

Year 3

Energy storage systems must include EU-manufactured battery cells and key components.

2027

66% of electric vehicles sold in the EU must use European-produced batteries.

2030 (Target Impact)

Cost gap between EU and Chinese battery cells expected to fall from 90% to ~30%.

The Cost-Security Tradeoff

The Industrial Accelerator Act forces a fundamental choice between cost efficiency and supply chain security. European battery cells currently cost 90% more than Chinese alternatives, a $41-43/kWh gap that translates directly to higher vehicle prices and energy storage system costs. Proponents argue this gap will shrink to 30% by 2030 as European manufacturers achieve scale and match Chinese efficiency levels. That still leaves a €500 per vehicle premium, a “sovereignty cost” European consumers and businesses will pay for reduced import dependence.

The employment implications are significant but unevenly distributed. Europe’s labor-intensive production model uses 125 workers per GWh compared to China’s 35, creating more jobs but also raising costs. The IAA projects 85,000 battery sector jobs created or preserved, concentrated in manufacturing regions that have struggled with deindustrialization. However, downstream industries that rely on affordable batteries—including automotive suppliers, energy storage developers, and renewable energy operators—face higher input costs.

The investment screening provisions target Chinese capital explicitly. Foreign investors from countries controlling more than 40% of global battery manufacturing capacity face majority ownership restrictions, mandatory technology transfer, and local employment quotas. This reverses the previous openness to Asian battery manufacturers, who received approximately €2 billion in EU state aid since 2021. The new framework ensures public support flows to facilities that create local value, but risks deterring foreign investment altogether if conditions prove too restrictive.

Europe’s Battery Strategy: Cost vs Security

Higher Costs

- EU battery cells cost ~90% more today

- €500 added cost per EV by 2030

- Higher labor intensity (125 workers/GWh vs 35 in China)

- Risk of slowing energy storage deployment

Strategic Benefits

- Reduced reliance on China (80% global production)

- 85,000 battery sector jobs

- €10.5B added automotive value

- 30.58M tonnes of CO₂ savings

Industry Reactions: Speed Versus Scale

Energy storage advocates have raised concerns about the timeline for BESS requirements. Dries Acke, Deputy CEO of SolarPower Europe, stated that “the requirements for battery energy systems are stricter and kick in too early” and “risk being counterproductive, especially given the urgent need to rapidly scale-up battery energy storage systems.” He emphasized that “battery storage is the absolute short cut to maximising Europe’s use of domestically produced renewable electricity and reducing Europe’s exposure to punishing fossil gas import prices.”

Aurélien Ballagny, Senior Policy Officer at Energy Storage Europe, echoed this concern, stating that “identified dependencies should be addressed through a realistic pathway for diversification, ensuring that the deployment of energy storage, and therefore renewables, is not slowed down or made more expensive.” The tension reflects competing priorities: building European manufacturing capacity requires time and scale, but Europe’s energy transition needs rapid deployment of storage systems to support renewable energy integration.

The European Solar Manufacturing Council expressed disappointment with related solar provisions, arguing the Act’s focus on cells and inverters falls short of creating a complete supply chain. Battery industry associations have been more measured, recognizing the need for policy support while warning against requirements that price European storage out of the market before domestic production can ramp up to sufficient scale.

IAA—A Necessary Risk?

The Industrial Accelerator Act represents a calculated bet on managed transition over market forces. Europe has decided that relying on Chinese battery imports creates unacceptable vulnerabilities, even if domestic production costs more. The 2025-2026 energy price spikes following Middle East escalation demonstrated the risks of fossil fuel dependence; the IAA extends that logic to clean energy supply chains.

The three-year timeline for battery cell requirements is tight but not unrealistic. Projects already in development, such as the ongoing gigafactory projects in Spain, France, or Hungary, will reach operational capacity by 2029-2030. The phased approach gives manufacturers time to adjust while signaling clear demand that can attract private investment. The alternative—voluntary targets without enforcement—has already failed under the Net Zero Industry Act.

The estimated €500 per vehicle premium by 2030 is a manageable cost spread across a vehicle’s lifetime. It amounts to less than 2% of an average electric vehicle’s purchase price, small compared to the volatility European consumers face from energy markets dependent on imported fossil fuels. If the cost gap narrows to 30% as projected, European battery manufacturers will have achieved sufficient competitiveness to survive without perpetual protection.

The real risk lies in implementation. European Parliament and Council negotiations could weaken requirements or extend timelines, undermining the demand certainty manufacturers need to justify capacity investments. Member states must also ensure permitting, infrastructure, and financing support keep pace with policy ambitions. Without coordinated execution, the IAA becomes another aspirational document rather than a catalyst for industrial transformation.

Final Take

The Industrial Accelerator Act commits Europe to building battery manufacturing capacity at higher cost than importing from China. The policy trades short-term price advantages for long-term supply security, betting that scale and efficiency improvements will narrow cost gaps to sustainable levels by 2030. Success depends on maintaining political will through the transition period, when higher costs will be visible but industrial benefits remain nascent. For the battery industry, the message is clear: European demand will increasingly flow to European production, with timing favoring manufacturers who can meet requirements within the phased schedule. The transition carries real costs, but Europe has decided the alternative—permanent dependence on a concentrated, geographically distant supply base—carries greater risk.